Current Challenges

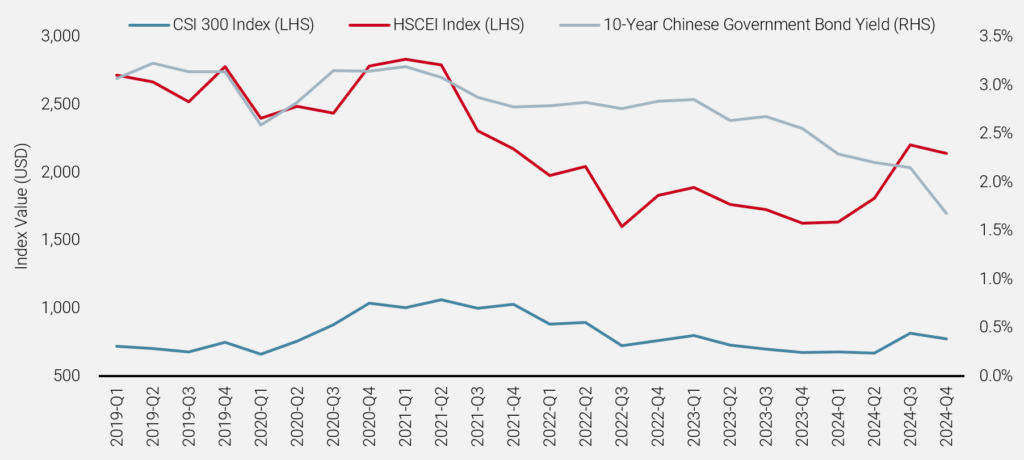

China’s economy has been battling multiple headwinds: a deepening property crisis, deflationary pressures, and weak domestic demand. In response, Beijing has rolled out a series of stimulus measures since the pandemic, hoping to reignite growth. Despite these efforts, the blue-chip CSI 300 Index remained stuck in a prolonged bear market, falling over 20% since 2020.

Last autumn, authorities unveiled some of their most aggressive interventions to date. The reserve requirement ratio (RRR) and the seven-day reverse repurchase rate were slashed, while the minimum down payment for second-home purchases was lowered. This initially triggered an intense—but short-lived—rally, as domestic investors briefly regained confidence in the government’s ability to boost demand.

Fast forward four months and market enthusiasm has fizzled. Fresh policy updates have failed to extend the rally, leading some investors to recall the déjà vu of 2022, when a major stimulus package initially lifted stocks, only for the market to drop 14% over the next six months. Today, deflationary fears and sluggish growth have pushed China’s 10-year bond yields to decade lows below 2%. Even multiple rate cuts from the People’s Bank of China (PBOC) have done little to lift equities. With property prices eroding consumer wealth, domestic investors now face fewer options for generating returns.