As we are now in a regime where interest rates should stay higher for longer, we believe our strategies should perform well for the coming quarters/years.

Looking at the full rate of interest rates cycle, we know our strategies tends to suffer during the first weeks/months when interest rates start to increase. However, this is usually short lived and then rising interest rates do not have much of an influence over relative performance.

Nonetheless, a regime where interest rates stabilise at a high level is usually favourable to our strategies as high interest rates penalise the valuation of high growth companies (given the value of their future earnings is strongly diminished by a high discount rate). Companies which are by nature more defensive, with less uncertainty around their earnings growth, are becoming very attractive for investors as visibility on the true value of their earnings is much greater.

The second effect is coming from leverage. Many companies usually attempt to benefit from low interest rates periods to boost their profitability by increasing leverage and using it either to fuel capex, or to return capital to investors through share buyback programs. However, when we shift to a high interest rate regime, those companies face a significant impact on the serving of their financial debt, combined with a more restricted ability to refinance their leverage because of tighter financial conditions. This is typically the type of companies our strategy seeks to avoid; hence our relative performance usually benefits from avoiding those ailing stocks.

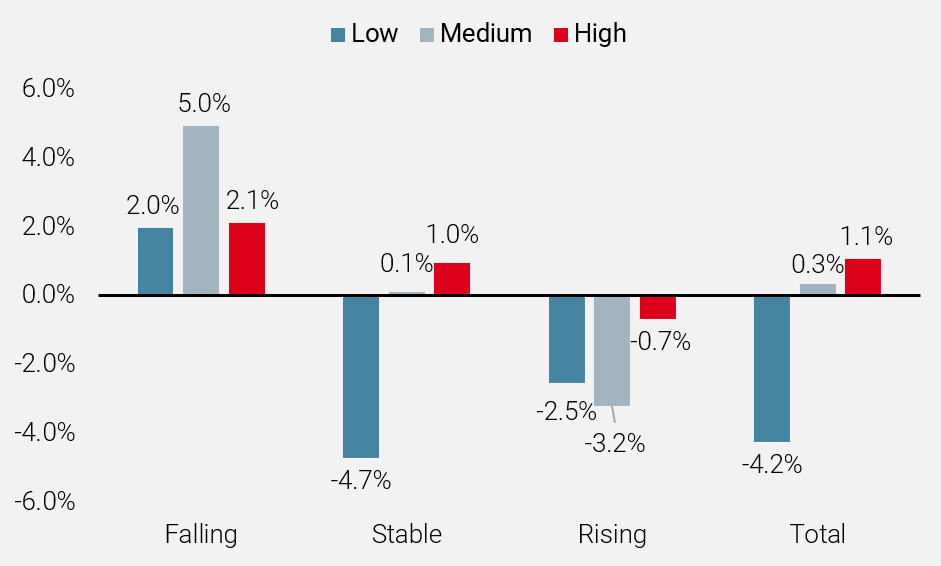

For example, below is the realised performance (average monthly excess return) of our European equity strategy during periods of low/medium/high interest rates, and also looking at the three-month trend (rising –stable – falling). We clearly see (Chart 10) that high interest rates create a positive regime, and falling interest rates are also very supportive.

Chart 10: Historical behaviour of our European strategy during various rate regimes